In general, selling your shares in the company that you own, you pay no tax.

Why?

When you own your business in Canada, assuming the company is a Canadian- controlled private corporation and at least 90% of its assets must be used in an active business in Canada, you can say the company is a qualified small business corporation (“QSBC”). What it means that shares of the company that you own qualifies for the capital gain deduction when it is disposed. For 2017, for each individual is entitle to a lifetime cumulative capital gain deduction of $824,176. So, a lot of business owners enjoy such tax exemption (paying no tax) when deciding to sell the company for retirement.

Simply speaking, there are three primary requirements for a QSBC:

1. A Canadian-controlled private corporation (CCPC);

2. Uses “all or substantially all” of its assets in an active business;

3. Carries on primarily in Canada.

A few things that business owners need to pay attention to:

- As each individual is entitled to a lifetime cumulative capital gains deduction of $824,176, you can enjoy taking advantage of this deduction in multiple times in lifetime as long as the gain realized in QSBC does not exceed the limit;

- The available capital gains deduction is also affected by other capital gains deductions previously claimed on any property; cumulative net investment loss (CNIL) account and an allowable business investment loss claimed previously;

- Watch out the redundant cash and portfolio investment sitting in the company’s books, those are considered non-active assets, which disqualify the company as a QSBC;

- A lot of people don’t pay attention to the ownership. Remember the share(s) must be owned by the individual, his spouse, common law partner, or partnership related to the individual.

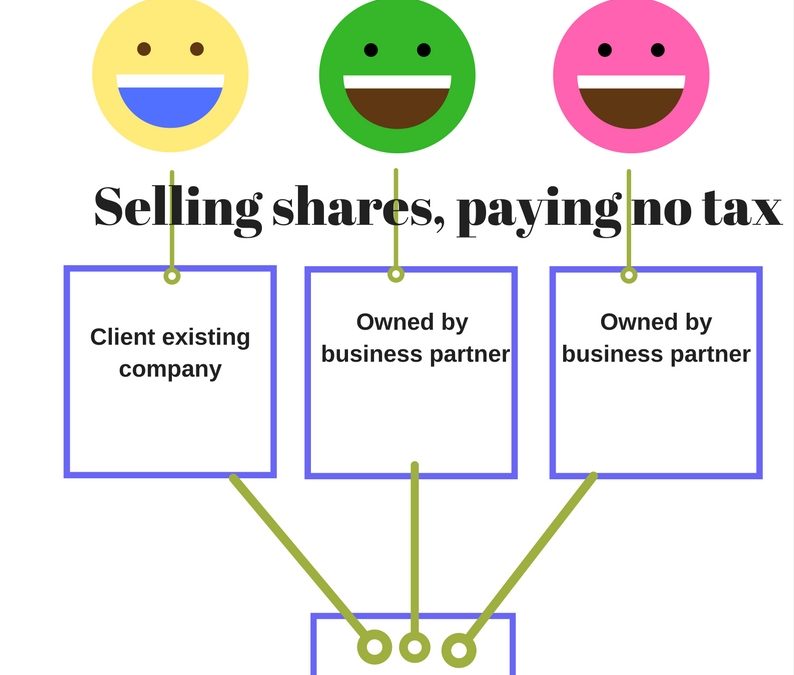

I came across a case that client plans to use its company to own an opco on a new venture with business partners (equal shares of the ownership of the opco) while client runs his separate business on his existing company. Here I assume both client’s existing company and the opco meet all the conditions for a QSBC during the years. There is an issue here. Is his existing company (as a shareholder of the opco) entitled to capital gain deduction when client wants to sell the shares of the opco only?

The answer is NO. Why? As explained in the points above, the shares of a QSBC must be owned by individuals.

The answer can be YES. This works only when client sells the share in his existing company along with the opco. But the question remains. Will the buyer be interested buying two separate businesses in the future? .

There are a few solutions recommended by tax professionals but really depending on the situations:

Amalgamation of the existing company and the opco prior to the disposition (will the partners agree?)

Client decides to conduct an asset sale for upward adjustment on the price to offset the tax impact resulting from asset sale (will the buyer agree?)

There are a lot of uncertainties in this case. The key question is always how you like to play around with business decision vs. tax planning, which decision comes first. It’s always a good idea to plan and assess the impact before the action. Future is a lot more controllable from that perspective. Do you think so?

Recent Comments