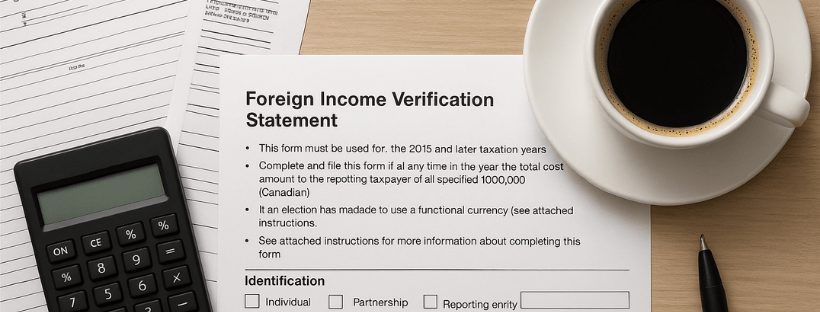

In Canada ,You must file a T1135 if you are a Canadian resident (for tax purposes) and at any time during the year you own specified foreign property with a total cost amount of more than CAD $100,000.

This includes (but is not limited to):

- Funds held in foreign bank accounts

- Shares of foreign corporations (even if held in a Canadian brokerage)

- Interests in non-resident trusts

- Foreign rental properties

- Debt owed by foreign entities (e.g., bonds)

- Certain foreign insurance policies

❗Note: This does not include:

- Foreign property used exclusively for personal use (like a vacation home)

- Canadian mutual funds or ETFs that hold foreign investments

- RRSPs, TFSAs, or other tax-sheltered accounts that hold foreign investments

This is a recent tax court case: a taxpayer was taken to Tax Court by the Canada Revenue Agency (CRA) because she filed her T1135 Foreign Income Verification Statements late for the years 2019 and 2020. These forms are required when a Canadian taxpayer owns foreign property worth over $100,000.

What Happened?

Ms. L owned U.S. investments through a Canadian brokerage account. This type of investment counts as “foreign property” under Canadian tax law. Because the total value went over the $100,000 limit in 2019 and 2020, she was legally required to file a T1135 form each year. She didn’t, and the CRA charged her a $2,500 penalty per year — the maximum allowed for this kind of error.

What Did Ms. L Say in Her Defence?

Ms. L agreed that she filed the forms late, but she argued that she shouldn’t have to pay the penalties because she had made an honest mistake and had tried to do her taxes correctly. She said she was diligent and did research to understand the rules herself.

Can You Avoid Penalties If You Tried Your Best?

Yes — sometimes. The judge explained that there is something called a “due diligence defence.” This means that if someone took reasonable steps to follow the rules but still made a mistake, the court might let them off the hook. The judge confirmed that this kind of defence does apply to late-filed T1135 forms.

So Why Didn’t Ms. L Win?

Here’s the problem:

Ms. L had made this exact mistake before. Back in 2012 to 2014, she also didn’t file her T1135s. Her accountant caught the issue in 2015, and they made a voluntary disclosure to the CRA to avoid penalties. At that time, she learned that U.S. investments in a Canadian account still count as foreign property.

After that:

She stopped using her accountant in 2018 because she no longer needed to file U.S. taxes (she had given up her U.S. citizenship). She started doing her own taxes using software and Google searches. She didn’t remember the details of the earlier disclosure or think to double-check whether she still needed to file T1135s. She didn’t ask her former accountant or revisit the past issue — even though her investments had changed significantly. She only realized the mistake when a new broker sent her a report in 2021 showing the value of her U.S. investments. At that point, she tried to do another voluntary disclosure — but the CRA rejected it because she had already used the same excuse years earlier.

What Did the Judge Decide?

The judge believed Ms. Laurie was honest and generally responsible with her taxes. But, because she had already made this same mistake once and been warned, a reasonable person in her situation would have taken extra care not to repeat it. In other words, she should have known better. The judge said:

“A reasonable person would have been put on alert to the risks and would have taken careful steps to make sure they did not fall into the same trap again.”

The Final Decision: Ms. L was not duly diligent, so she must pay the $5,000 in total penalties ($2,500 for each of 2019 and 2020). Her appeal was dismissed.

✅ Key Lesson:

If you’ve already made a tax mistake once, the courts expect you to be more careful in the future. Even if you’re honest and well-intentioned, repeating the same error — especially after professional help — makes it very hard to avoid penalties later on.

Recent Comments